Payout protection cover

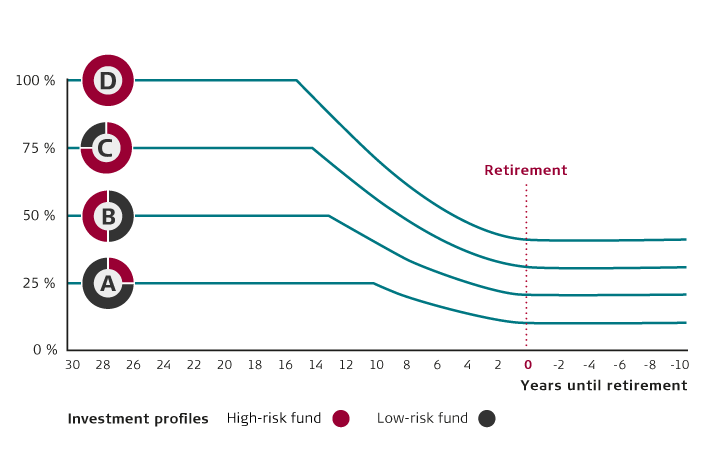

Individual customers with PFA’s market rate product, PFA Plus, who have chosen the investment concept PFA Invests and have selected investment profile A or investment profile B (includes both the savings option PFA Plus and PFA Climate Plus) can also select the product called Payout protection cover for their plan.

A payout protection cover ensures that your pension payouts will generally not drop below a certain level. If you have decided to add payout protection cover, then, as a rule, we will add this cover to your savings for ten years up to your expected retirement. This takes place via part of your savings being gradually invested in some special funds - so-called long-duration funds - with a very low risk.

From the moment where we begin to phase in payout protection cover on your savings, you can keep an eye on what proportion of your savings is invested in long-duration funds and you can also keep an eye on the secured level of cover for your payouts on an ongoing basis. The savings in long-duration funds represent the amount needed to ensure the value of the part of your pension that is linked to payout protection cover.

The special duration funds that are used for payout protection cover are, under normal market conditions, expected to generate a lower return than the High-risk fund and the Low-risk fund, which are the funds that your savings are allocated to without payout protection cover. This means that your pension payouts will usually be expected to be lower if you have linked payout protection cover to your plan. In some cases, the payouts will be significantly lower. Under current market conditions with the historically low interest rates, we even expect that there will be losses (negative return) on the part of your savings allocated to the long-duration funds.

Please note that the payout protection cover can in some cases lapse or be changed. You can read more about this in your terms and conditions of pension.

Environmentally sustainable investments

The investments that this financial product is based on do not consider the EU criteria for environmentally sustainable economic activities.

Categorisation under the EU’s Sustainable Finance Disclosure Regulation (SFDR)

Payout protection cover does not promote environmental or social characteristics and does not have sustainability as its target pursuant to Section 6 of the EU’s Sustainable Finance Disclosure Regulation (SFDR).